About three weeks ago, we got a letter from our individual insurance carrier (Anthem, the only show in town) informing us that the high deductible HSA plan that we currently have will not be available in 2014. The next best thing they say, is their Core DirectAccess with HSA. Our monthly premiums would double, from $682 to $1,361. All this, they say, is because of the Affordable Care Act.

Yikes! That’s what I call sticker shock. So I took a look at the ten plans that they offer on their web site, and sure enough, can’t do much better than $1,361. I don’t know how I expected millions more people to be insured, and all the people with pre-existing conditions to be covered, without somebody paying more. But double?

So, moving along, I went to healthcare.gov out of curiosity. What a train-wreck, but let’s not throw the baby out with the bath water. I eventually managed to set up an account and then took a look at what was available.

As expected, the only plans were from Anthem, but there was something different, they were cheaper. It found that I can get a Bronze DirectAccess with HSA for $1,070. That’s still 67% over our old plan but a long way from the doubling that was quoted by Anthem.

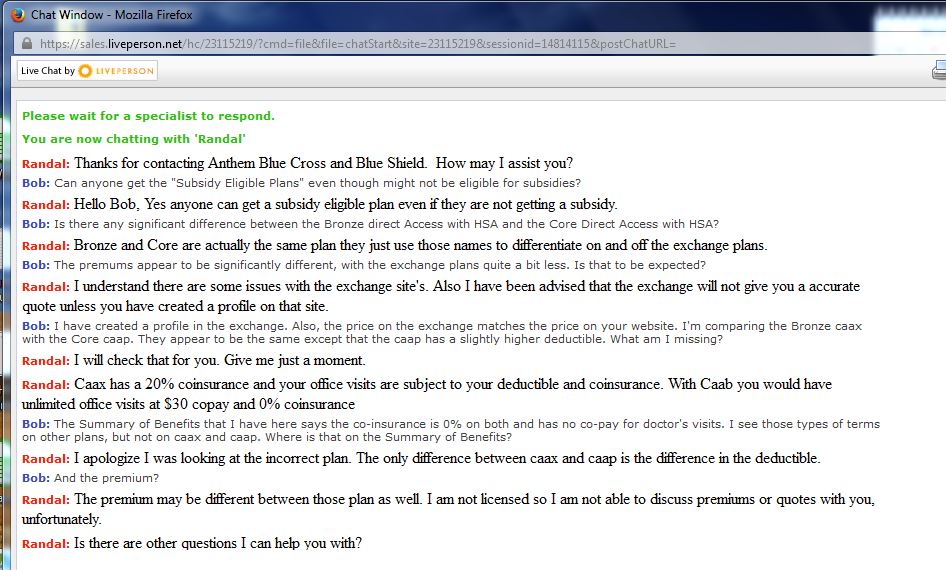

I went to online chat with Anthem and asked about the differences between the two plans. Here’s the transcript: They trash the exchange, misquote the plans, and avoid talking about price. But I was persistent, and eventually found out that the only difference, besides price (which “he isn’t allowed to talk about because he’s not a licensed agent”), is that the higher priced Core plan direct from Anthem has a higher deductible. That’s right, the more expensive plan has a higher deductible. Go figure.

They trash the exchange, misquote the plans, and avoid talking about price. But I was persistent, and eventually found out that the only difference, besides price (which “he isn’t allowed to talk about because he’s not a licensed agent”), is that the higher priced Core plan direct from Anthem has a higher deductible. That’s right, the more expensive plan has a higher deductible. Go figure.

At the end of the day, we can’t have our cake and eat it too. Our old policy was the result of the insurance company cherry-picking the population for healthy people, and excluding people that were likely to actually need significant health care. We were fortunate to be healthy enough to qualify for healthy people only insurance, but that’s not the case for everyone. I think it’s the right thing to do, and many people qualify for subsidies that reduce their cost.

What I learned was that Anthem can’t be trusted not to take advantage of the confusion and blame it on Obamacare. Yet at the end of the day, the exchange and Obamacare’s requirement of a standardized benefits description allowed us to find the significantly lower priced equivalent policy.

The only reason I can come up with for the lower price on the exchange is that there may be limits imposed by Obamacare on policies sold through the exchanges. I’ll be curious to see what happens if the exchanges ever attract serious competition to Anthem’s long standing lock on the New Hampshire individual insurance market.

Under Obamacare, I thought that we would save an average of $2500 per family. and could keep our current insurance if we wished.. My experinece is similar to yours. I am getting wsick and tired of being lied to when ever it suits our so called leaders agenda.

Well Dick, I don’t think your experience could be similar to mine in that I believe you and your wife are eligible for Medicare. I would be delighted to buy into Medicare at say, the per-capita cost plus 10%.

I’m not familiar with the context of the $2,500 per family savings average, and I can’t imagine how there could be any basis for comparison, given that the pre Obamacare pool of insured was only healthy people, and the post includes virtually everyone. In any event, averages can be achieved while some pay more. The jury is still out on the final average costs.

My complaint is with Anthem, who appear to be trying to protect their golden goose by misleading me as to my options, and with the website, which is a truly epic blunder.

Throughout all of this, there has never been a credible alternative offered by the opposition. Simply continuing to have a health care system that excludes the unfortunate is not a price I’m willing to pay for keep my lucky-to-be-healthy low premiums.

Single payer catastrophic major medical for all would be a good compromise, along with subsidized clinics for preventive care. Then eliminate the two tier system where the uninsured pay three times as much for services as the insurance companies pay for their insured (and tell people up-front what those costs are). They are not selling insurance, they are selling their political clout.